What is closing cost?

Closing costs refer to additional fees you must pay after the purchase of a home. Taxes and fees that are related to real estate transactions are included. These are paid by both the buyer as well as the seller depending on which party is responsible for the specific process.

These closing costs consist of both one-time fees as well as the initial installments you will pay each month along with your mortgage. These recurring costs may include homeowners insurance and property tax payments, and can vary from lender to lender.

Some of these charges are fixed while others are calculated based on your loan amount. You'll likely have to pay an application fee, attorney fees, and courier charges.

The typical closing costs of a buyer

Closing cost will vary by state and county property tax rates. These fees can include the title company fee, escrow charge, appraisal fee and record filing.

What is the average cost of refinancing?

Closing expenses for a refinanced loan are generally lower, but still have to be included. The Loan Estimate that lenders send to buyers three days after applying for a loan will include estimated closing costs.

This estimate should not only be accurate, but it should also be easy to understand. Ask questions when you're not sure about something.

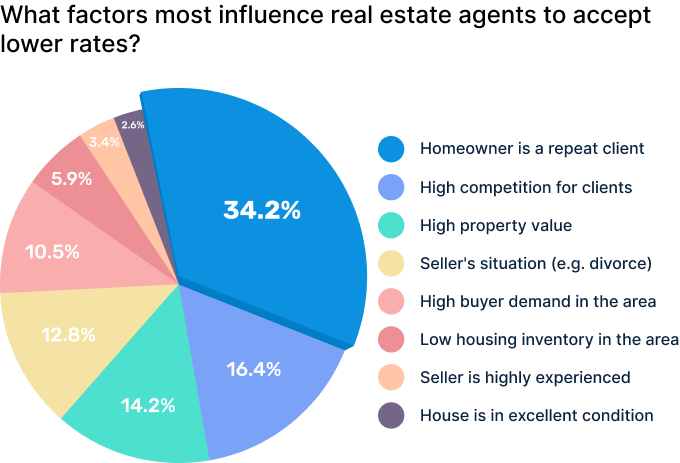

What are the closing cost for home sellers and buyers?

The closing costs that home sellers have to pay include broker's fees and transfer taxes. Home sellers are often required to pay prepaid mortgage interest, home inspection and pest control fees.

If the service provider is willing to lower their fee, they can negotiate this cost. They can also ask for a seller credit, which is money contributed by the seller to cover a portion of the buyer's closing costs.

How to reduce closing costs

Shopping around for the right mortgage is the best way to avoid these costs. You should consider your credit rating, debt-toincome ratio and down payment before applying for a mortgage.

It will also give you more time to do research on the price of homes in your preferred neighborhood or city. Before making a decision, you can compare the fees and rates of different lenders.

A seller's mortgage tax recording fee and a transfer of title fee are also payable by the seller. They usually amount to 1.825% of home sale price. These are often overlooked by buyers, but they're a big deal and can add as much as 2% to the price of a resale home.

FAQ

How long does it take for my house to be sold?

It depends on many factors, such as the state of your home, how many similar homes are being sold, how much demand there is for your particular area, local housing market conditions and more. It may take up to 7 days, 90 days or more depending upon these factors.

Can I get another mortgage?

Yes, but it's advisable to consult a professional when deciding whether or not to obtain one. A second mortgage is typically used to consolidate existing debts or to fund home improvements.

What are the 3 most important considerations when buying a property?

The three main factors in any home purchase are location, price, size. Location refers to where you want to live. Price refers how much you're willing or able to pay to purchase the property. Size refers how much space you require.

How do I calculate my interest rate?

Market conditions can affect how interest rates change each day. The average interest rate for the past week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. If you finance $200,000 for 20 years at 5% annually, your interest rate would be 0.05 x 20 1.1%. This equals ten basis point.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How do you find an apartment?

Finding an apartment is the first step when moving into a new city. This involves planning and research. This includes researching the neighborhood, reviewing reviews, and making phone call. There are many ways to do this, but some are easier than others. Before renting an apartment, you should consider the following steps.

-

Data can be collected offline or online for research into neighborhoods. Online resources include Yelp. Zillow. Trulia. Realtor.com. Local newspapers, real estate agents and landlords are all offline sources.

-

See reviews about the place you are interested in moving to. Yelp and TripAdvisor review houses. Amazon and Amazon also have detailed reviews. You can also check out the local library and read articles in local newspapers.

-

To get more information on the area, call people who have lived in it. Ask them about what they liked or didn't like about the area. Ask if they have any suggestions for great places to live.

-

Consider the rent prices in the areas you're interested in. Renting somewhere less expensive is a good option if you expect to spend most of your money eating out. You might also consider moving to a more luxurious location if entertainment is your main focus.

-

Find out information about the apartment block you would like to move into. How big is the apartment complex? What price is it? Is the facility pet-friendly? What amenities does it have? Can you park near it or do you need to have parking? Do tenants have to follow any rules?